Optimization of the Japan permanent residency (2024)

On 14 June 2024, the 213th Ordinary Session of the Diet passed a draft amendment to the Immigration Control and Refugee Recognition Act, which includes the establishment of a training and employment system (Ikusei-Shuro) for the purpose of developing and securing human resources, and was promulgated on 21 June. The main principle of the amendment is to establish a new training and employment system in place of the Technical Intern Trainee system (Ginou-Jisshu) for foreign workers.

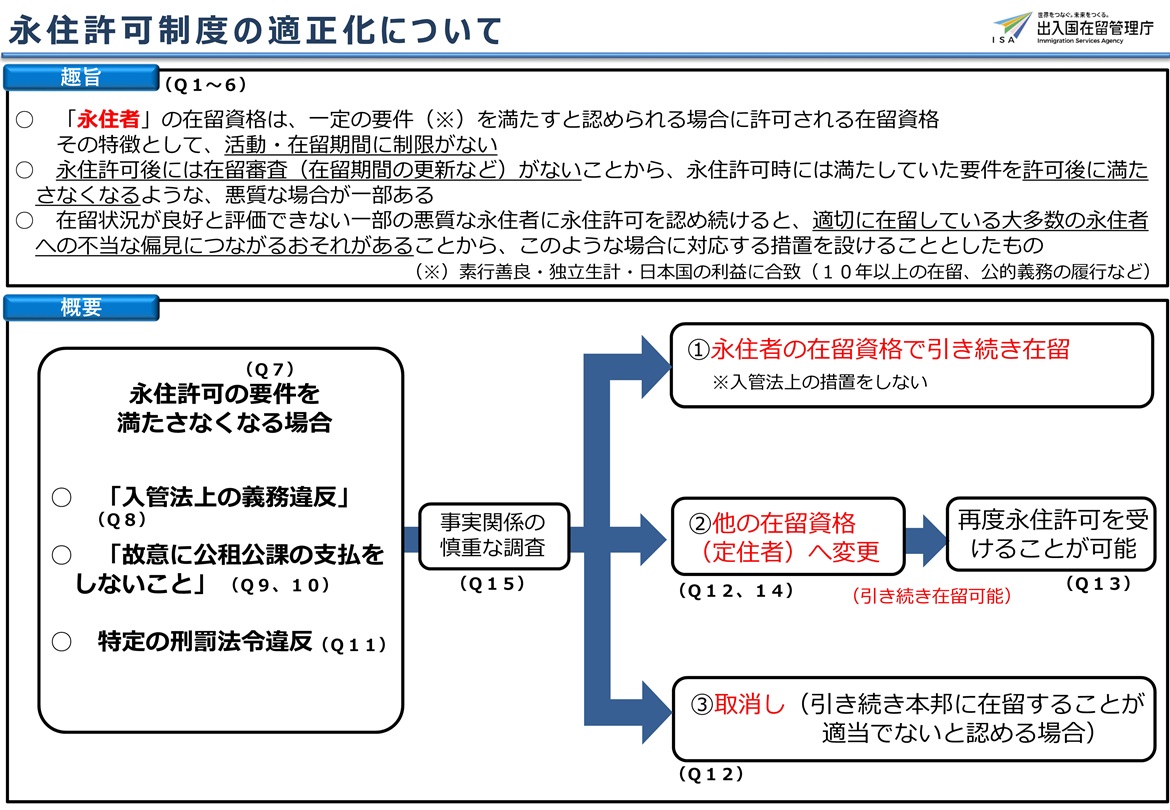

The revised law also allows for the revocation of a permanent residence permit (PR) if a foreigner deliberately fails to pay taxes. The Japanese authorities have announced that the law is intended to optimise Japan’s immigration control system, as it has been pointed out that some foreigners with permanent residency have not fulfilled their official obligations. While it is possible to revoke a permanent residence permit if a foreigner deliberately fails to pay taxes, etc., a supplementary provision has been added stating that, when revoking the permit, due consideration must be given to the living conditions of the foreigner.

Let’s take a closer look at this optimization of the permanent residence permit system.

First, the status of ‘permanent resident’ is a residence status granted to foreigners living in Japan if they are deemed to meet certain requirements. One of its characteristics is that there are no restrictions on activities or period of stay.

Foreigners with visas other than permanent resident status are forced to face inconveniences such as not being able to stop working. As a story made famous by a popular Japanese entertainment TV programme, foreigners who come to Japan on a professional visa to make the Indian curry cannot do any other work as long as they are in Japan and must continue to make curry until they obtain permanent residency.

This is a very advantageous permanent residency for foreigners, but on the other hand, the Japanese authorities are concerned that there are some malicious cases where foreigners no longer fulfil requirements that were met when they were granted permanent residency, as there is no residence examination (renewal of period of stay) after the permanent residence permit has been granted. The government authorities claim that if they continue to grant permanent residency to some malicious permanent residents whose residence status cannot be assessed as good, it may lead to unfair prejudice against the majority of permanent residents who are residing properly, and therefore they have decided to establish clarification of the requirements for permanent residence permits, a measure to deal with such cases. It says that the clarification of the requirements for a permanent residence permit is a measure to respond to such cases.

What does the clarification of the permanent residence permit requirements entail?

Will new requirements be added, raising the bar for permanent residence permit applications and making the assessment requirements more stringent?

No, nothing will change for foreigners who are about to apply for permanent residence. As all foreigners who are about to apply for permanent residence know, ‘compliance with obligations, payment of taxes and public dues’ will now be a matter of course. This amendment to the law does not add any new requirements for a permanent residence permit, nor does it make the requirements for the permit stricter.

The clarifying measure is to clarify the requirement in the current Immigration Act for a permanent residence permit that “the person’s permanent residence is in the interests of Japan” as “compliance with obligations, payment of taxes and public dues, etc.” in the law. Taxes and public imposts refer to taxes and other public contributions such as social insurance contributions.

Foreigners who are already ‘permanent residents’, but not foreigners who are about to apply for permanent residence, should therefore be careful. In the very old days, there was a time when it was possible to pass the permanent residence examination even if you were not a member of the Japanese pension scheme. Permanent residents who have not paid into the Japanese pension system should be wary. Also, be careful if you have stopped paying into the pension system because you have acquired permanent residence. Permanent residents who say they have claimed a lump-sum withdrawal payment also cannot rest easy.

These may fall under Article 22-4(1)(viii) of the revised Immigration Act, ‘wilfully failing to pay taxes and dues’. Willful failure to pay taxes and public dues means that the taxpayer is aware that he/she is obliged to pay the tax or public dues, but dares not to do so. For example, this is assumed to be the case when a person knows that there are taxes and public dues to be paid and has the ability to pay, but does not pay the taxes and public dues.

On the other hand, if a foreigner is unavoidably unable to pay due to illness or unemployment, it is difficult to accept that the foreigner himself is responsible for the situation and the right of permanent residence is not supposed to be revoked. In these cases, it is better to go to the pension counter of the city/ward office and apply for exemption as soon as possible.

And even in the unlikely event that you fall under the grounds for revocation of your right to permanent residence, the decision on whether or not to revoke, etc. will depend on individual and specific circumstances, such as the circumstances that led to the non-payment and the state of the permanent resident’s response to the demand, etc.

What specific cases are envisaged when a person does not ‘comply with his/her obligations’? If a permanent resident inadvertently fails to carry his/her residence card or fails to apply for renewal of the validity period of his/her residence card, will his/her status of residence also be revoked?

Failure to comply with obligations stipulated by law refers to failure to fulfil, without just cause, obligations that permanent residents are required to comply with under the Immigration Act, which are not stipulated as grounds for deportation, but for which compliance is guaranteed by penalties.

In this regard, it is not specified what cases constitute non-fulfilment of obligations. However, it is reassuring to note that the revocation of status of residence is not envisaged if, for example, a person inadvertently fails to carry his/her residence card or fails to apply for renewal of the validity period of his/her residence card.

The right of permanent residence may also be revoked in the case of a violation of penal laws and regulations as stipulated in Article 22-4(1)(ix) of the revised Immigration Act.

The violations of penal laws and regulations stipulated here are specifically limited to certain serious violations of penal laws and regulations, such as theft, fraud, extortion and murder under the Criminal Code and manslaughter under the Act on Punishment of Acts Causing Death or Injury by Dangerous Driving of Motor Vehicles, and all of these offences are intentional.

Therefore, a person who causes a traffic accident and is punished for manslaughter by negligent driving is not covered by the law.

The Road Traffic Act is not included in the penal statutes stipulated as grounds for revocation, so if you are punished for a violation of the Road Traffic Act, you are not covered in the first place. The punishment must also include a custodial sentence, so if you are fined, you are also not subject to the law.

However, even permanent residents may be deported on grounds of deportation if they have been sentenced to a prison sentence of more than one year, regardless of the nature of the offence.

If you have any concerns or problems with the payment of taxes and public dues, please consult with your city or ward office, and if you have any concerns about your own permanent residence, please also consult with the Immigration Bureau or FRESC (Foregn Residents Support Centre).